Commodity prices and input costs are key considerations this year.

⋅ By H. Scott Stiles ⋅

University of Arkansas, Division of Agriculture

Rice or soybeans — or both? Many Mid-South growers are still wrestling with that decision. Deciding on the optimal crop mix for 2022 is complicated by a number of variables from relative crop prices and the outlook for each, to input costs and yield expectations.

Market fundamentals

Beginning with some thoughts on the rice market, new crop rice prices during the month of January are the highest they’ve been since 2014 with September 2022 futures trading between $14 and $14.50 per hundredweight (cwt). Given this price strength, it is becoming more likely the Mid-South will see year-to-year stability in rice acres. Planting time weather and soybean price direction will also play key roles in determining rice acres. No doubt too, growers will see higher input costs. However, the rice market is sending a clear signal as we start the year with tighter ending stocks.

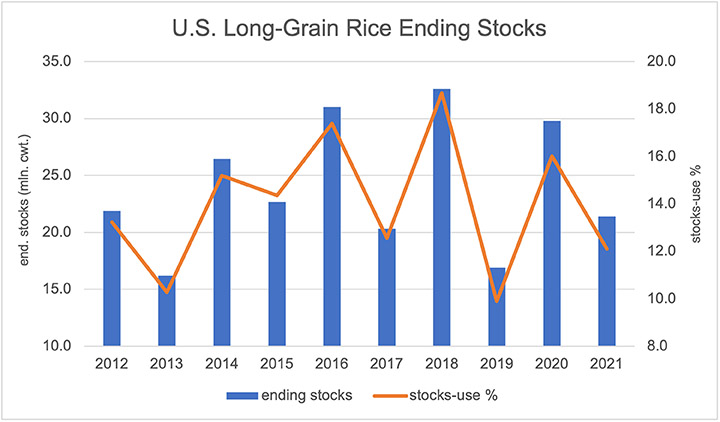

Despite record rice yields in Arkansas, Missouri and Mississippi, U.S. long-grain production was down 15% in 2021 on lower acreage. As a result, ending stocks are expected to drop in 2021/22. Long-grain ending stocks are currently projected at 21.4 million cwt.; down 28% from last year. This equates to a stocks-to-use ratio of 12.1% — below the previous five and 10-year average of 14%.

The U.S. Department of Agriculture also projects total supplies of long-grain to decline nearly 17 million cwt. in the current marketing year to 198.3 million. Historically, the United States has better export market participation in years with total supply at or above 200 million cwt. To maintain export market share, the futures market and basis are trying to keep rice competitive with other grains.

Given relatively low stocks-to-use in the U.S. long-grain balance sheet and historically high prices in competing commodities, one would be hard pressed to come up with a factor that would reduce rice prices in the early months of 2022. However, if I had to put one wet blanket on the rice outlook, it would have to be the possibility of USDA dialing back its long-grain export projection. USDA’s current long-grain export target for 2021/22 is 64 million cwt.; not quite 2% below last year’s 65.1 million.

By comparison, U.S. long-grain sales and shipments through mid-January are running 10% behind last year. Long-grain milled rice sales are up compared to a year ago, due to the 120,000 tons sold to Iraq last July. More than offsetting the export gains in milled rice is a 23% decline in rough rice sales. This sharp drop is due in large part to the “once-in-a-decade” sales the United States made to Brazil last year. And U.S. rough rice sales to Venezuela are down about 128,000 tons year-on-year.

Battle for acres

In 2022, soybeans will be a key competitor for rice acres in the Mid-South. Corn and cotton are competing for acres as well and lending some price support to rice. November 2022 soybean futures began to surge higher in early December (2021) and continued into January on poor crop conditions in key areas of South America. For much of January, the November soybean contract has traded in the range of $12.75 to $13.35 per bushel. Corn and cotton have followed soybeans higher with new crop contracts moving above $5.80 and 98 cents, respectively.

With September 2022 rice futures trading at 7-year highs, it is apparent rice prices are at least attempting to provide the same relative profitability as soybeans. In this era of extreme commodity price volatility, few will offer up a price projection for the upcoming year. That being said, prior to planting, new crop rice prices appear likely to remain at levels that prevent a large shift from rice to soybeans in the upcoming year. More information about planting intentions will be released March 31 in USDA’s Prospective Plantings report.

Input costs

Higher input costs will be a major consideration in 2022 planting decisions. Compared to a year ago, variable costs for a conventional hybrid rice production system have increased almost $230 per acre or 34%. These cost increases are based on budgets published by the University of Arkansas in early December 2021.

Sharp increases in production cost have been driven largely by fertilizer and fuel. Many crop chemicals have increased in cost over the past year as well. Assuming an average yield of 190 bushels per acre, rice prices would need to increase by roughly $1.20 per bushel to maintain the same return as in 2021.

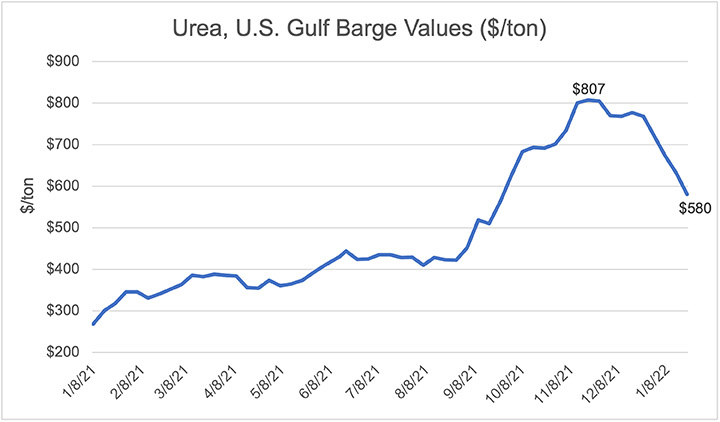

Rice prices still have some work to do to offset increases in input costs. However, competitiveness with soybeans may get a boost by way of lower nitrogen costs if recent trends continue. Since mid-November, urea barge values at the U.S. Gulf have fallen by more than $220 per ton. This is obviously great news for producers who have remained on the sidelines and waited for fertilizer prices to decrease.

From conversations with Mid-South growers and suppliers, it appears the price decline in urea barge values at the Gulf translated to the retail level. By mid-to-late January, pre-pay urea offers near $675 per ton were reported in some areas — significantly lower than prices plugged into budgets near the end of 2021.

In the University of Arkansas 2022 crop budgets, an average urea price of $850 per ton is used in the rice budgets published in early December. Reducing the cost of urea to $675 per ton trims off nearly $29 per acre in fertilizer expense. If urea prices remain well below the late 2021 highs, that could factor into planting decisions, particularly with rice, corn and cotton impacted most by fertilizer cost increases over the past year.

On a final note, keep in mind the current fall bids for rice and soybeans are well above long-term averages. Pre-harvest hedging of a portion of 2022 production seems warranted, particularly if some input purchases have already been made. In times when commodity prices are historically high, the responsibility of price risk management falls entirely on the producer.

Since the Price Loss Coverage (PLC) program was initiated in 2014, the $14/cwt reference price for long-grain rice has exceeded the season average producer price in each marketing year thus far. This streak appears it could be broken in the 2022/23 marketing year.

As commodity and input prices hover near historical highs, make the necessary revisions to crop budgets and marketing plans. Before returning to the field this spring, remove some stress by identifying profitable price levels and a marketing strategy that protects your farm business.

H. Scott Stiles has been an Extension ag economist with the University of Arkansas for 22 years.