• By Scott Stiles •

Rice futures pushed beyond key resistance this week. In trading Tuesday, the November contract managed to close above $13.80 for the first time since Aug. 16. Nearby chart resistance is at the August high of $13.92. A sizable cut to production in the Sept. 10 U.S. Department of Agriculture outlook has helped push rice prices about 25 cents per bushel higher.

Rough Rice Nov ’21 (ZRX21)

Fresh fundamental news has been sparse this week. However, harvest activity is picking up in the Mid-South region and providing more yield information. Market momentum has turned higher this month and the continued improvement in Gulf exports should be price supportive.

On Thursday, cash basis for delivery to mills was 18 under November futures with bids at $6.04/bu. Basis at driers around eastern Arkansas was 25 to 32 cents under futures with bids in the $5.91 to $5.98 range.

Export sales:

The U.S. Gulf continues to recover from Hurricane Ida with more grain export facilities expected to resume operations next week. U.S. export sales of all grains continue to reflect the logistics complications at the U.S. Gulf, with sales and shipments below year-ago levels.

Long-grain rough rice sales for the week ending Sept. 16 dipped to a marketing year low of only 200 tons. The only rough rice sale last week was 200 tons to Guatemala.

Long-grain milled sales and shipments were also down from the previous week’s totals. There were no sales reported to Haiti or Iraq for the week. Total sales of 4,916 mt went mostly to Canada, Costa Rica, and Saudi Arabia.

Over the first six weeks of the 2021/22 marketing year, rough rice sales have totaled 349,066 metric tons versus 320,603 mt sold during the same period last year. With stronger sales year to date to Mexico, Guatemala,\ and Costa Rica, rough rice sales are currently 9% ahead of last year.

Carried largely by the 120,000 mt sold to Iraq, total long-grain export sales (rough, brown and milled combined) are running 39% ahead of last year.

Crop progress:

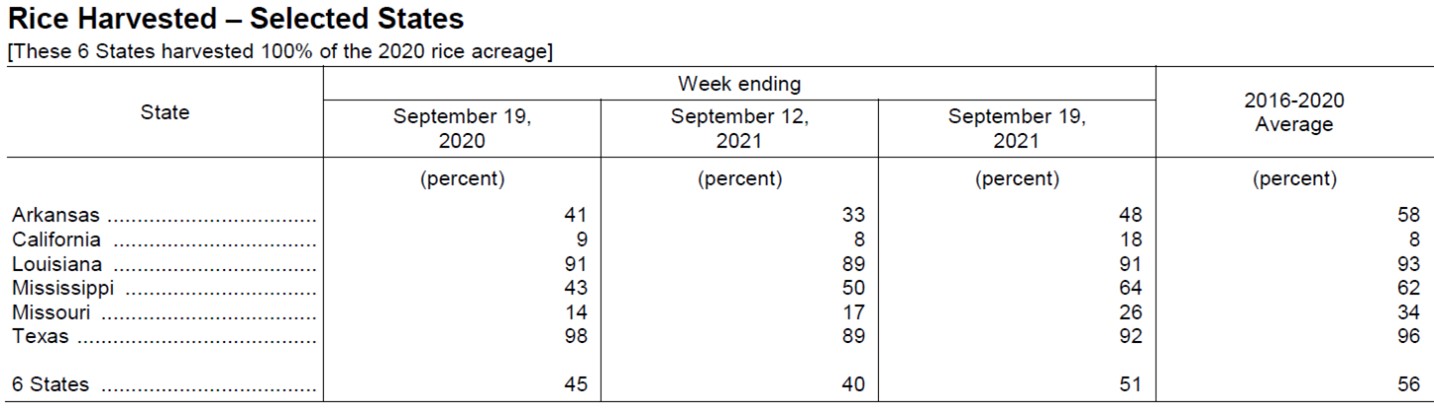

In Monday’s Crop Progress, U.S. rice harvest was 51% complete as of September 19th; slightly behind the 5-year average of 56 percent. Arkansas was near the halfway mark. The Deep South is wrapping up, with Louisiana and Texas at 91 and 92% harvested, respectively. Mississippi was 64% harvested; 2 percent ahead of their average pace. Missouri was at 26% harvested. Fortunately, tropical storm activity has remained well out in the mid-Atlantic this week. The near-term forecast for the Mid-South is clear and warmer, allowing steady harvest progress.

Yield forecasts:

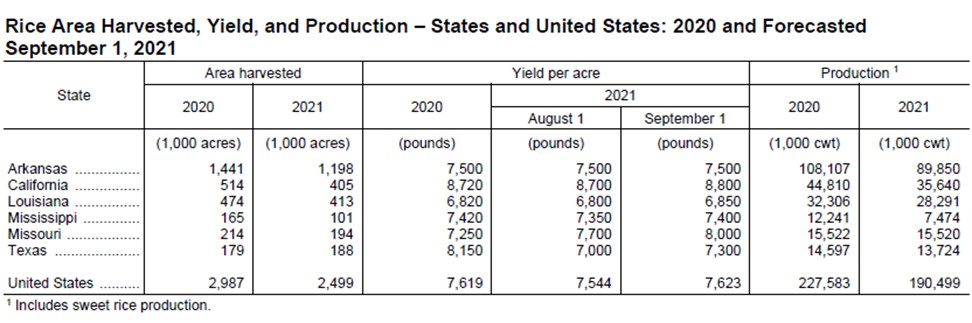

USDA increased average yield estimates in September for all states, except Arkansas. Arkansas’ state average yield is projected to be 7,500 pounds (166.7 bu./ac.); unchanged from the August estimate and last year.

Missouri’s average yield is projected to be the highest in the Mid-South at 8,000 pounds (177.8 bu./ac.); up 750 pounds or almost 17 bushels from last year.

Input costs:

We are already getting calls this month for the 2022 budgets. With the sharp increases in fertilizer and fuel this year, growers have been thinking about what they will plant next year.

Will higher input costs impact rice acreage in 2022? Will growers turn more heavily to soybeans, a crop that requires less fertilizer and lower input costs overall? Commodity and input price direction over the coming months will help answer those questions.

As mentioned last week, we have the 2022 wheat budgets available and should have the spring planted crop budgets available in early October.

Fertilizer prices continue to work higher. This week an October urea barge traded at $600/ton fob New Orleans—the highest since May 2012. The slow return to normal the U.S. Gulf is still causing problems in both production and movement of fertilizers and crop chemicals.

Bayer’s glyphosate manufacturing plant in Louisiana has been shut down since August 28th. We are told the Luling, Louisiana, plant provides all the active ingredient for Bayer’s Roundup produced in the United States. In addition, imports of glyphosate shipped into the Port of New Orleans are down 71% from a year ago.

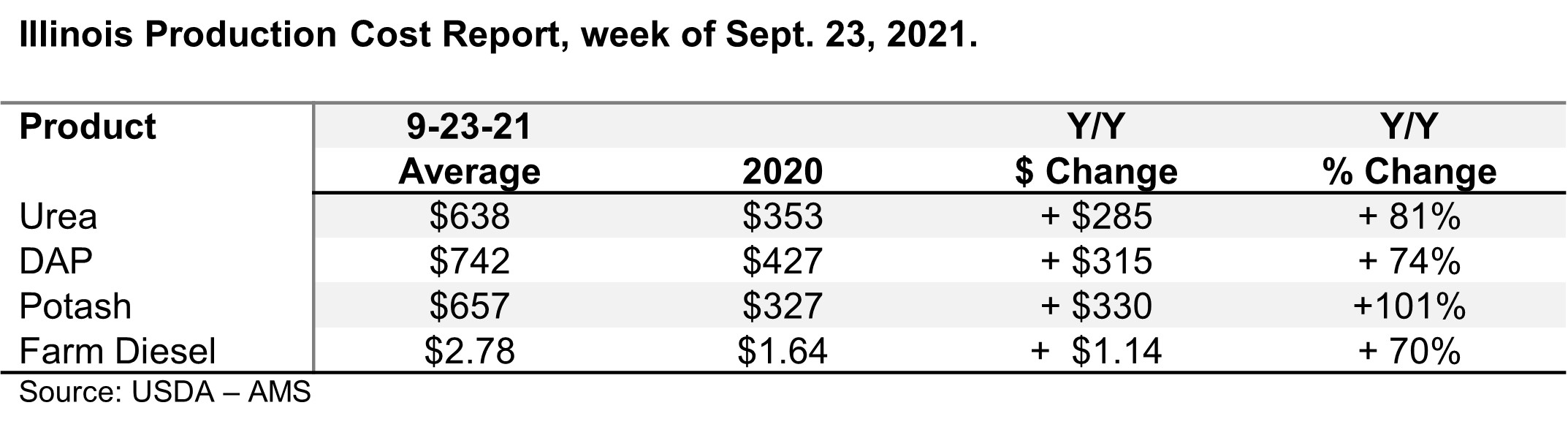

Below is partial listing of some inputs from a survey that USDA AMS releases every two weeks. These are average retail prices from ag input dealers in Illinois. Although retail fertilizer prices in Arkansas may differ slightly, the key takeaway is the price trend over the past year.

Urea is 81% higher, DAP 74% higher, Potash has doubled and farm diesel is up 70% compared to last year.

We hear from industry sources that price increases for urea, phosphates and potash are not showing any signs of a top. The fertilizer market continues to be too volatile to predict with a mix of logistical and political issues affecting prices.

The spike in natural gas prices is another factor driving up nitrogen fertilizer costs. No doubt it will be challenging to lock-in inputs with local suppliers, but get the process started as soon as possible.

Scott Stiles is a University of Arkansas Extension agricultural economist. He may be reached at [email protected].