⋅ BY RYAN LOY ⋅

University of Arkansas Division of Agriculture

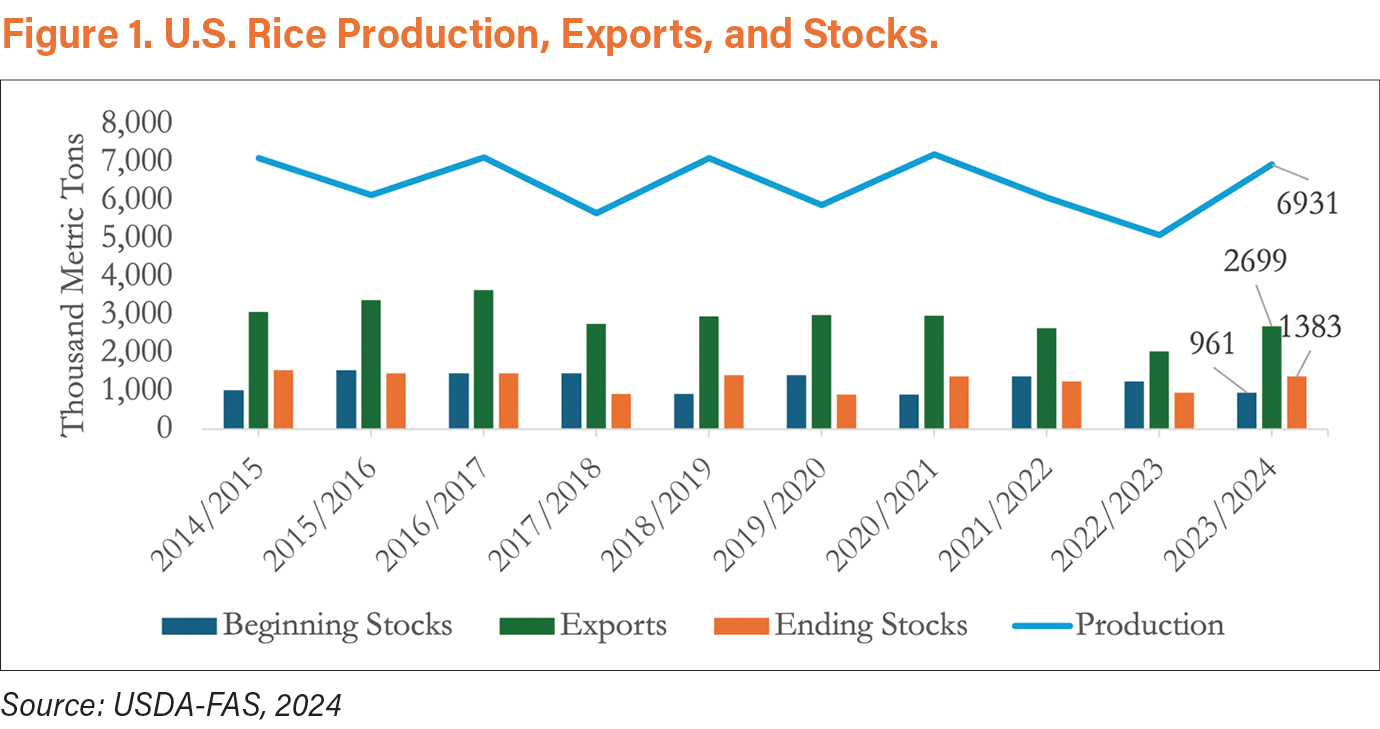

Following two consecutive years of decline (see Figure 1), United States rice production increased to roughly 2.9 million acres in 2023. In 2022 and 2023, the world was consuming more rice, which showed up in the long grain rice Marketing Year Average Prices (MYAP) of $16.70/cwt and $15.7/cwt, respectively. Production increases in 2023 (see Figure 1) followed 2022 high prices that were last seen around harvest of 2013. Fast forward to March 2024, where the then current November rough rice futures contract was trading at $14.66/cwt. The November contract price decline has been steady since late December 2023 but has recently begun to increase again ($0.44/cwt since Feb. 27, 2024).

There was an extreme multi-year drought in California during the 2022 growing season. During this time, California rice producers could not plant nearly 300,000 acres, due to a lack of water for irrigation. Arkansas (a state that almost exclusively grows long-grain varieties) responded by increasing its acreage of medium-grain rice by 55,000 acres in 2023. However, California rebounded in 2023 and surpassed 500,000 acres of medium-grain rice. An abundance of medium-grain rice could hinder any upside price potential if the demand for medium-grain remains at normal levels.

An Eastern Pacific El Niño has also disrupted off-season rice production for Thailand, Burma, and Indonesia. These countries rely on off-season production to improve their stocks and export amounts. Now, they face extreme drought, impacting yields and production, and may not have enough carry over and ending stocks to bring rice to the global economy. The U.S. Department of Agriculture forecasts that global rice production for 2023/24 will exceed 2022/23 by only 0.1% (583,000 metric tons). Thus, the El Niño conditions are poised to further tighten global rice supplies in these major exporting countries.

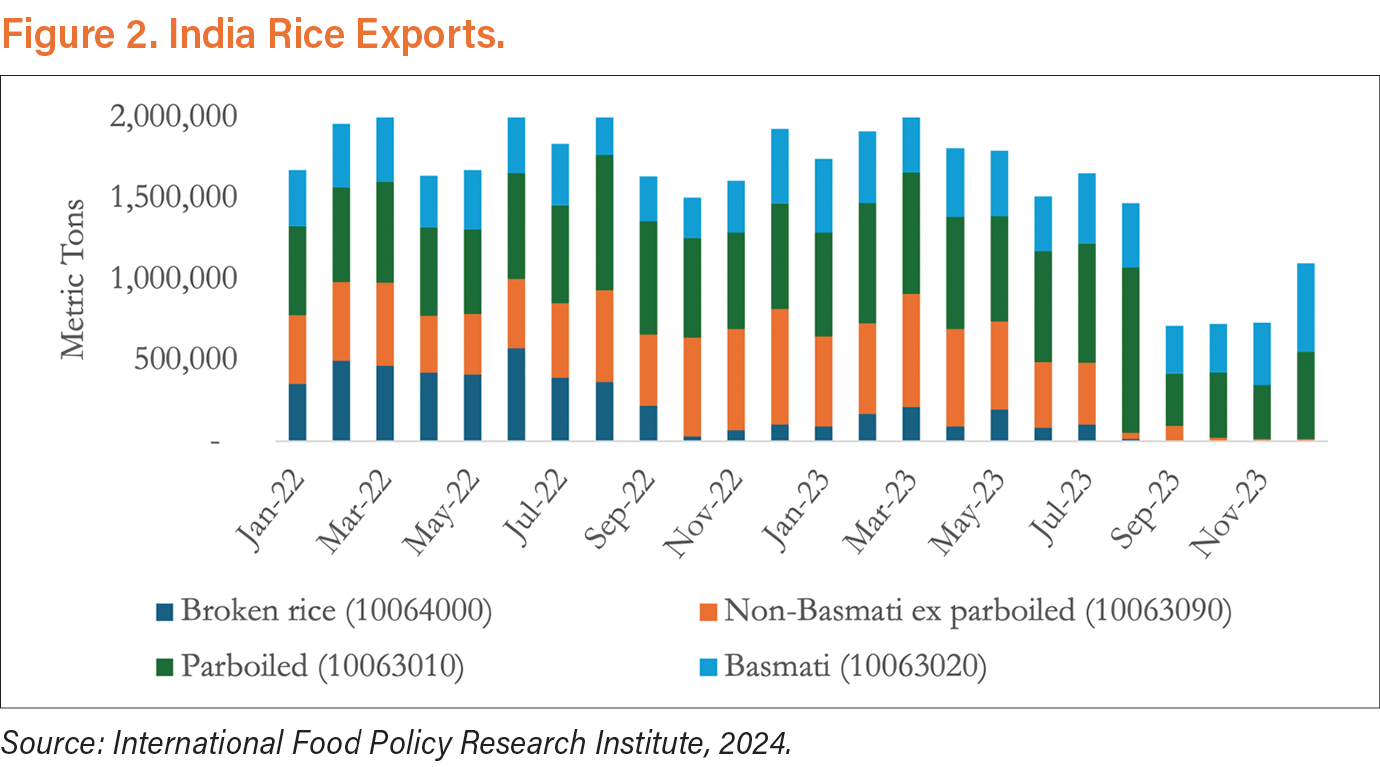

Global rice supplies are also strained from India’s July 2023 export ban on non-basmati rice. The ban was implemented to help lower domestic rice prices and to ensure rice availability in India. On a global scale, India accounted for nearly 40% of all rice exports in 2022, further showing the global impact of India’s exports. Referring to Figure 2, the ban forced a 93% decline in non-basmati rice exports between August and November of 2023. Importing countries are now forced to turn to alternative suppliers to meet their rice demands. It’s worth noting that India is currently in an election year and it’s doubtful the ban would be lifted before a general election in April or May. If the ban is lifted post-election, watch for Indian rice to flood the market and put further downward pressure on global rice prices.

Overall, the 2024 rice market will be extremely sensitive to ongoing global conflicts, weather, government policies, and shipping issues such as low water levels in the Panama Canal, a potential return to low water levels in the Mississippi River, and conflicts in the Red Sea. There could continue to be opportunities in the export market should Mississippi River levels stabilize during harvest and if India’s export ban continues. With it being early in the season, it’s worth highlighting that on a per-bushel basis, the recent soybean-to-rice price ratio for November 2024 delivery was 1.78 ($11.73/$6.60). This ratio has continued to decline since 2021, when the ratio was 2.41. All to say that the relative prices of other commodities, such as soybeans, are in a similar declining price environment as rice.